Last month, B4B Payments welcomed leading travel businesses to its London headquarters for a roundtable on the future of payments in the sector. The afternoon created space for open conversations, offering valuable insights and practical ideas on how the industry can move beyond outdated systems and adopt smarter, more transparent financial solutions.

A recurring theme was the need to shift away from cash-heavy processes that are costly, inefficient, and difficult to manage across multiple markets. Clients and B4B experts explored how greater visibility of spend, backed by the right technology, can give finance teams more confidence while keeping financial risk under control.

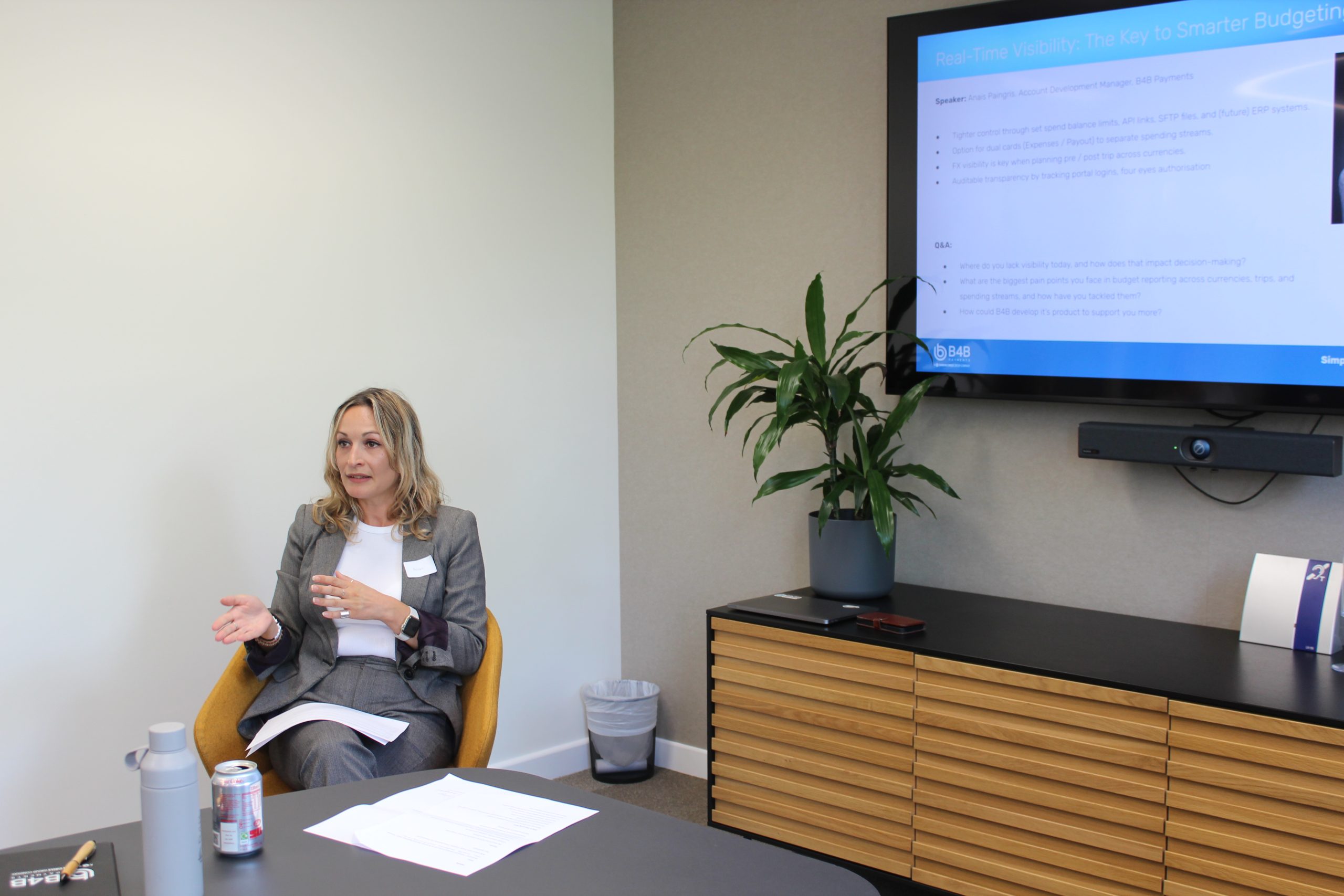

Adding perspective from the B4B side, Director of Accounts and Partnerships Tim Robson spoke about the challenges of lagging travel spend data, whilst also showcasing differences in global card and cash use. He showed how modern card solutions can help operators gain oversight, reduce reliance on cash, and even simplify issues such as paying tour directors outside payroll. Building on this, Account Development Manager Anais Paingris emphasised the benefits of tighter spending controls through our system, from auditable transparency with new authorisation, to FX visibility. Together, their contributions sparked an engaged dialogue on how B4B Payments’ technology can ease long-standing industry problems.

What stood out throughout the roundtable was the quality of discussion. Clients spoke candidly about their current pain points, including heavy reliance on ATMs and cash in some markets, as well as the difficulty of preventing fraudulent spending. Equally, they offered constructive feedback on how B4B Payments could further enhance its solutions to support evolving business needs.

The session reinforced a common understanding: while the travel sector continues to recover, especially following the COVID-19 pandemic, sustainable growth depends on more innovative financial systems. By embracing technology and reducing cash dependency, travel businesses can take greater control of their operations and ensure they are well-positioned for the future.

B4B Payments thanks all attendees for their valuable insights and contributions, which made the roundtable a forward-looking exchange for everyone involved.

Skip to the content

Skip to the content